While an exciting opportunity, becoming a director or officer of a company carries with it a number of duties, the extent of which many directors may not fully appreciate or understand. The majority of duties are set out in the Corporations Act 2001 (Cth), however, there are many other sources of obligations such as Federal and State legislation, tax legislation and work health and safety (WHS) regulations which directors need to comply with.

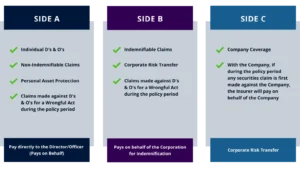

| If a company has the financial capacity to offer a comprehensive deed of indemnity to the director, the contractual agreement between the company and the director is most important. This is still considered the best first line of defence to help cover or indemnify a director against personal liability. Side B cover (Company reimbursement) of the D&O policy can reimburse the company where it has provided indemnity to the Directors. | Directors & Officers Insurance assists in situations where the company’s financial situation cannot accommodate a deed of indemnity; for example, the company is insolvent or near insolvency. It also serves to cover a class of liabilities where indemnification is prohibited. |

Duties of Australian Company Directors

| There are a number of legal obligations that come with being the director of an Australian company. These are in place to protect the stakeholders of the company and must be adhered to.

Some of the legal obligations a director must follow include the duty to: |

For a comprehensive list of directors duties, see the Corporations Act 2001. |

Vicarious Liability

| In the case of a company breaching relevant laws or legislation, the director may become personally liable in some circumstances. This is called vicarious liability and may be imposed upon the director if they were in force at the time the company breached the law. Vicarious liability can be brought about by breaches of various laws, including the following:

|

|

Due Diligence of Company Directors

| Directors must undertake due diligence to identify any risks in the company and manage them appropriately. Regarding directors’ duties and vicarious liability, due diligence can help to establish protocols and processes to ensure the smooth running of a company. Undertaking due diligence not only reduces errors and harm to stakeholders but can also help protect directors from liability. | A keen understanding of duties, WHS and other legislation, is needed so the director can ensure the company is following all protocols to reduce risk and liability. D&O Insurance can help to minimise the risk of financial penalty in many circumstances, but not all. |

Consequences of Breaching Directors Duties

| Breaching Directors’ duties results in some serious consequences, including both Civil (monetary penalty imposed as a result of civil proceedings) and Criminal (criminal sentence, penalty or fine imposed) penalties:

Breaches resulting in Civil Penalties

| Breaches resulting in Criminal Penalities

Most D&O insurance policies include a general exclusion for claims:

|

When Indemnity is Prohibited

| A company is able to financially protect directors against some liabilities, but not all. Indemnification and exemption of an officer or auditor by a company is limited by or prohibited in certain circumstances under s199A of the Corporations Act.

When Indemnities for liabilities are not allowed (other than legal costs)

A company or a related company must not indemnify a person (directly or through an interposed entity) against any of the following liabilities incurred as a director of the company:

A key concern for directors when defending an action is whether the company can assist with indemnity for legal costs. S199A(3) prohibits this in the following circumstances: | When Indemnities for legal costs are not allowed

A company or a related company must not indemnify a person against legal costs incurred in defending an action for a liability incurred as a director of the company if:

|

A typical D&O policy

| In most instances, a director or officer will be covered by the Side A component of the D&O Insurance policy (KBI D&O policy structure) for general liabilities and legal costs where the company may not indemnify. There is a prohibition in Section 199B of the Corporations Act which prohibits a company from paying premiums for an insurance policy which indemnifies a director against liability for:

| The central theme of the prohibitions under s 199A and s 199B of the Corporations Act is that they focus on conduct towards the company itself or conduct accompanied by lack of good faith, intention, and wilful breach. |

Work Health and Safety Breaches

| The legislation regarding insurance and WHS differs slightly across Australia’s states and territories as they each have their own WHS Acts. Be sure to familiarise yourself with your state’s specific legislation.

In 2020 New South Wales amended their WHS Act to include the prohibition of entering into an insurance policy that intends to indemnify the person from their liability to pay a fine or an offence under the WHS Act. This law extends to insurers, making it illegal to issue a policy covering WHS breaches. Western Australia has followed suit by overhauling their Act, prohibiting insurance against WHS breaches.

WA’s Work Health and Safety Act 2020 brings with it the creation of the criminal offence, Industrial Manslaughter, which requires the following elements:

| Western Australia and South Australia are the most recent states to introduce a specific charge of Industrial Manslaughter, bringing them in line with Queensland, the ACT, Northern Territory and Victoria. New South Wales does not specifically have a charge for Industrial Manslaughter, but their WHS Act has been updated to include Manslaughter offences linked to workplace incidents. Tasmania is now the only state without an Industrial Manslaughter offence.

Directors have a duty to exercise due diligence to ensure a PCBU (Person Conducting a Business or Undertaking) complies with their obligations. Basically, the director is responsible for ensuring the company is keeping its workers safe. The duty imposed is a positive duty requiring a proactive approach by directors to ensure they comply with the obligations under the legislation. Failure to comply now brings harsher consequences with the prohibition of insurance and introduction of Industrial Manslaughter, with a maximum imprisonment term of 20 years for individuals and a fine of $5M, or a $10M find for a Body Corporate.

|

D&O insurance

| D&O Insurance is becoming increasingly difficult to obtain at competitive pricing. Cover is being scaled back due to reductions in capacity and changes in underwriting guidelines. As legislation develops, Directors & Officers will need to examine the structure of their D&O Insurance policy at every renewal. It is essential to revisit the gaps that may exist between their Deed of Indemnity and the D&O Insurance, keeping a careful eye on any areas of exposure. | At KBI, we can guide you when structuring your policy in a way that brings optimal risk minimisation. Talk to KBI about your D&O Insurance requirements.

|

We are a specialist insurance brokerage with an emphasis on adding value to our clients by helping them make an informed decision. Our approach combines that of an insurance broker and consultant, where we focus on providing expert advice to our clients while customising their insurance program and risk management solutions.

Since starting in 2013, KBI is constantly growing and becoming a leader in the Australian market. Our primary point of difference is that we don’t try to be all things to all people. We work in niche areas, where we can tailor an offering, advice and broker support to meet the specific area’s needs.

latest news

Related Articles

Association Insurance

Why Do Associations Need a Tailored Insurance Program?

Associations play a key role in many industries. They represent the shared interests of professionals, businesses, and communities. Associations operate in dynamic […] {{ post.title }}>Read More

Why Do Associations Need a Tailored Insurance Program? Read ArticleCyber Blog

Strengthening Your Business with Comprehensive Cyber Insurance Solutions

In this article, we provide some key insight into the current cyber insurance landscape including how insurers are responding to increasing risks […] {{ post.title }}>Read More

Strengthening Your Business with Comprehensive Cyber Insurance Solutions Read ArticleBusiness Insurance

Safeguarding Business Continuity: Learning from the Optus Outage

In an era where connectivity is the lifeblood of businesses, the recent Optus outage in Australia served as a stark reminder of […] {{ post.title }}>Read More

Safeguarding Business Continuity: Learning from the Optus Outage Read Article