There is an ever-increasing list of matters which Directors need to consider in risk management and decision making. In this article, KBI considers two emerging risks and the impact they are having on D&O Insurance: Climate Change and Human Rights issues.

Climate Change

| The 4th edition of the Corporate Governance Recommendations (released in February 2019) included in its recommendations to listed companies a recommendation that they disclose whether they had any material exposure to environmental or social risks and their approach to managing those risks. The following reference appears as part of Recommendation 7.4:

The Council would encourage entities to consider whether they have a material exposure to climate change risk by reference to the recommendations of the Financial Stability Board’s Task Force on Climate-related Financial Disclosures (“TCFD”) and, if they do, to consider making the disclosures recommended by the TCFD.

Companies who choose to make this disclosure should analyse the potential impact of a number of climate related scenarios (one example being rising temperatures) on the organisation and refer to the plans adopted to mitigate against the risks. | This reporting framework is becoming a topic for consideration, not only by company directors, but also by retail and institutional investors. For example, superannuation funds are influenced by transparent disclosure on climate risks, as well as companies’ policies and strategies in approaching these risks. This scrutiny indicates that these are investment risks that will not be ignored in the investment assessment process, no different to other considerations such as financial metrics and business systemic risks.

Many companies are leading the charge with their TCFD reporting in financial disclosures, as well as aligning executive remuneration and key performance targets with the overall strategy. Institutional investors who are members of collaborative groups, such as the Investor Group on Climate Change (https://igcc.org.au/) and Climate Action 100+ (http://www.climateaction100.org/), are engaging with companies to require them to consider the impact of climate change and release appropriate and comprehensive disclosure about these risks. |

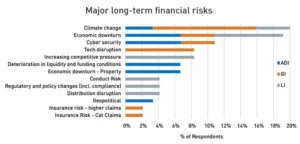

*An APRA survey undertaken last year across Australian banks, general and life insurers listed climate change as the number one long-term financial risk, ahead of economic downturns and well ahead of cyber security. ADI – Australian Deposit-taking Institutions, GI – General Insurers, LI – Life Insurers

Human Rights

| With this year’s introduction of the Modern Slavery Act, directors will also be considering disclosures pertaining to human rights and assessing the risk of modern slavery at any point in their supply chain or operations. The International Labour Organisation believes that 21 million people worldwide are forced labourers, with half of those in the Asa-Pacific region – a fact that Australian companies will not be able to ignore. | Currently, entities with more than $100 million in revenue will be required to report disclosures relating to human rights due diligence and publish annual modern slavery statements on an online central register. |

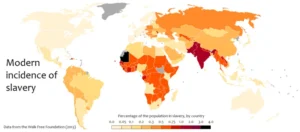

*Infographic showing the estimated percentage of population in slavery, by country, as of 2013/14. https://commons.wikimedia.org/wiki/File:Modern_incidence_of_slavery.png

ASIC High Level Recommendations

| ASIC has released a media guideline (available on ASIC website) which provides some high-level recommendations to listed entities, to assist them in their disclosure around climate risk. These include:

|

|

Directors and Officers Insurance

| D&O insurers often respond to significant market events (i.e. the historic and current Royal Commissions) by increasing premiums and including new endorsements to D&O insurance policies. This is generally because these policies reflect the prevailing governance concerns at any particular time. With the increased scrutiny on companies’ disclosures around sustainability risks, including climate change, we would expect to start seeing premiums increase for companies operating in what are perceived as more “risky” business activities, including resources (mining and oil & gas) and industrial operations. We would also anticipate more customised endorsements relating to climate change/emissions and exclusions designed to carve out any responsibility for errors by companies in relation to their TCFD reporting. | Certain insurers, for instance IAG, have made a conscious decision to limit their exposure to entities with carbon intensive industries. Their Climate Action Plan released in October 2018 noted that less than 1% of their premiums covered carbon intensive industries in FY18. This has clear implications for companies operating in this sector. |

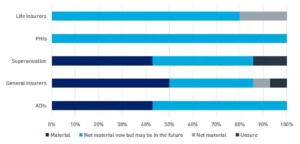

*A recent survey conducted by APRA in 2018 across Australia’s largest banks, general, life and health insurers, and superannuation funds found the banking, general insurance and superannuation industries reported the highest awareness of climate risks. Life and private health insurers were less likely to be taking steps to understand the risks, and less likely to view the risks as material to their businesses.

| With increased retail and institutional shareholder attention to these matters, we would expect to see an increase in the potential for securities claims and class actions due to incomplete, inadequate or erroneous reporting. On the flip side, we would like to believe that companies operating in less risky environments/industries and who report against TCFD guidelines and align executive remuneration with climate related measures, will benefit from more competitive premiums and less onerous endorsements.

In a similar vein, with the introduction of the Modern Slavery Act, we believe that retail and institutional investors will be expecting enhanced disclosure by the larger companies obligated to report in accordance with the legislation. However, this will place pressure on smaller Australian listed entities who have any exposure through their supply chain and/or their operations, to make appropriate and comprehensive disclosure. This will then demonstrate that their board is considering this an important business risk and is giving clear guidance on the due diligence conducted by the company, as well as the risk mitigation strategies the company is adopting. Failure to do so will most likely result in increasing scrutiny by shareholders, regulators and other interested parties. Any public censure by regulators or queries and corresponding share price drops may well expose the company to the threat of a derivative class action.

Corrs Chambers Westgarth, in its insight “A new era of climate change litigation in Australia”, identified the key matters which have historically been litigated on (and will continue to be litigated on). These included: | “…challenges to decisions by governments and other regulatory bodies to approve projects and developments which may have significant direct or indirect greenhouse gas emissions. The most obvious of these are projects such as coal mines, coal-fired power stations and gas exploration… Over time, greater focus may fall on projects with direct and indirect emissions that have not yet been as much of a focus of disputes. Those might include, for instance:

In the event that investors suffer a loss which they perceive could be attributed to inadequate disclosure by the board/management of their climate change risks, we believe this could result in a D&O claim. The claim could arise in a number of scenarios:

D&O Insurance is complex and the changing governance framework is making it even more so. Insurers respond to emerging risks quickly and it’s important to stay on top of the important considerations for your D&O policy and keep your broker informed. |

We are a specialist insurance brokerage with an emphasis on adding value to our clients by helping them make an informed decision. Our approach combines that of an insurance broker and consultant, where we focus on providing expert advice to our clients while customising their insurance program and risk management solutions.

Since starting in 2013, KBI is constantly growing and becoming a leader in the Australian market. Our primary point of difference is that we don’t try to be all things to all people. We work in niche areas, where we can tailor an offering, advice and broker support to meet the specific area’s needs.

latest news

Related Articles

Association Insurance

Why Do Associations Need a Tailored Insurance Program?

Associations play a key role in many industries. They represent the shared interests of professionals, businesses, and communities. Associations operate in dynamic […] {{ post.title }}>Read More

Why Do Associations Need a Tailored Insurance Program? Read ArticleCyber Blog

Strengthening Your Business with Comprehensive Cyber Insurance Solutions

In this article, we provide some key insight into the current cyber insurance landscape including how insurers are responding to increasing risks […] {{ post.title }}>Read More

Strengthening Your Business with Comprehensive Cyber Insurance Solutions Read ArticleBusiness Insurance

Safeguarding Business Continuity: Learning from the Optus Outage

In an era where connectivity is the lifeblood of businesses, the recent Optus outage in Australia served as a stark reminder of […] {{ post.title }}>Read More

Safeguarding Business Continuity: Learning from the Optus Outage Read Article