In order to answer this question, there are some fundamentals of D&O Insurance that should be understood.

Table of Contents

| Who Shares the Policy? What’s Covered in the Policy? What does Aggregate Limit mean? | What is the Structure of the Policy? Range of Factors to Consider When Setting the Limit Setting the Limit |

Key Insights

The D&O insurance limit of indemnity is a shared aggregate limit covering directors, officers, and the company where Side C applies.

D&O limits fund defence costs, settlements, and court-awarded judgments, which can rapidly erode the aggregate limit during a policy period.

Policy structure typically includes Side A (individual protection), Side B (company reimbursement), and Side C (entity securities liability).

Company size, market capitalisation, regulatory environment, insolvency risk, and merger and acquisition exposure are key drivers when setting D&O limits.

Availability and pricing constraints in a hardened D&O market can materially influence the achievable limit, regardless of board preference.

Who Shares the Policy?

| The policy limit is a shared limit for Insured Persons, this covers Directors and Officers (C-Suite management) and the company (if Side C is present). |

What’s Covered in the Policy?

| The limit of liability includes settlements and court awarded judgements and defence costs, which would otherwise need to be paid by the company or its executives. |

What does Aggregate Limit mean?

| The aggregate limit is the limit of liability available to each individual claim as well as all claims in the aggregate ie one large claim could erode the entire limit for the policy period and the aggregate limit typically doesn’t have a reinstatement. |

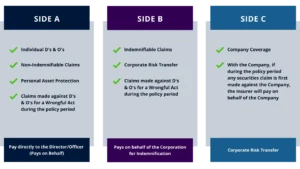

What is the Structure of the Policy?

| A typical D&O policy includes the following covers: |

|

|

There are a range of factors to consider when setting the limit

| ➤ Public / Private and Market Capitalization Generally speaking, the larger and more sophisticated a business the higher the risk, however there are some private companies that should consider a higher limit based on the degree of exposure of a particular project or enterprise they carry out. ASX top 100/200 are obviously the main targets for class action law suits and disgruntled minority shareholders.➤ Percentage Owned by Insiders Where directors and significant associated shareholders hold a large percentage of the issued share capital this may affect the decision on the limit. If directors hold a large proportion of the issued capital it may be argued that this reduces the scope and potential quantum of damages by claimants. Generally D&O insurers will include an endorsement aimed at excluding internal disputes between insiders for example the major shareholder exclusion (sometimes with a board seat). This excludes cover for the major shareholder suing the board or the company as they are expected to be helping direct the company and would be typically considered insiders.➤ Peer Group Where possible (because generally the policy information is confidential) it is useful to refer to the limits that companies in the peer group are purchasing for a guide to what limit is appropriate. KBI has access to peer group data that can benefit boards when picking a limit.

➤ Regulatory Framework

➤ Company’s Capacity to Retain Risk | ➤ Insolvency Risk At certain times in the company’s development the dependency on outside equity or debt may increase the risk of insolvency. At these times the company may consider a higher limit is justified. Certainly, the Directors and Officers might consider whether the company would be able to fulfil its indemnification obligations in the foreseeable future.➤ Merger & Acquisition Exposure The company’s growth plans may affect the limit decision. If the company’s strategy includes growth by acquisition or places them in circumstances where they may be subject to merger or acquisition themselves, they may consider a higher limit as these are inherently riskier activities.➤ Cost / Budget This can be linked to the company’s capacity to retain risk and also the cost per $1mil of coverage. With insurers’ pricing fluctuating as we enter a harder insurance market, the limit chosen often becomes a commercial decision of what limit of risk transfer is viable for the board/company.

➤ High / Low Risk Industry or Jurisdiction

➤ Availability |

Setting the Limit

| Once the above considerations have been taken into account we believe that setting the limit is a process reached between the board and an experienced broker. The interplay of the market capitalisation of the company, the free float of shareholders and average damages settlements (including defence costs) are all taken into consideration when reaching what we consider to be a minimum limit for the Board. Once this is identified the broker needs to work to secure the best available terms for the Board’s requirements. | Given the challenging insurance market and the likelihood of significant changes to the company’s business (for example in light of COVID and the overall economic downturn), we recommend that the Board revisit the limit every year in conjunction with an experienced D&O broker. |

We are a specialist insurance brokerage with an emphasis on adding value to our clients by helping them make an informed decision. Our approach combines that of an insurance broker and consultant, where we focus on providing expert advice to our clients while customising their insurance program and risk management solutions.

Since starting in 2013, KBI is constantly growing and becoming a leader in the Australian market. Our primary point of difference is that we don’t try to be all things to all people. We work in niche areas, where we can tailor an offering, advice and broker support to meet the specific area’s needs.

latest news

Related Articles

Association Insurance

Why Do Associations Need a Tailored Insurance Program?

Associations play a key role in many industries. They represent the shared interests of professionals, businesses, and communities. Associations operate in dynamic […] {{ post.title }}>Read More

Why Do Associations Need a Tailored Insurance Program? Read ArticleCyber Blog

Strengthening Your Business with Comprehensive Cyber Insurance Solutions

In this article, we provide some key insight into the current cyber insurance landscape including how insurers are responding to increasing risks […] {{ post.title }}>Read More

Strengthening Your Business with Comprehensive Cyber Insurance Solutions Read ArticleBusiness Insurance

Safeguarding Business Continuity: Learning from the Optus Outage

In an era where connectivity is the lifeblood of businesses, the recent Optus outage in Australia served as a stark reminder of […] {{ post.title }}>Read More

Safeguarding Business Continuity: Learning from the Optus Outage Read Article